My latest article for Worthwhile Magazine™ tackles a tricky area of appraising: understanding the different levels of value. This is one of the most confusing elements of appraising that I spend a lot of time discussing with clients, so I wanted to cover the subject in an article that could reach and help a much broader audience. The following is my article or you can also read it online at Worthwhile Magazine™:

“One of the most challenging things to wrap my head around during my formal training to be an appraiser was that value and worth as we popularly understand it in our culture are completely relative. There is immense curiosity regarding the question “what’s this worth?” but an appraiser’s answer is usually some form of “it depends.”

Value exists in the presence of its context in a specific level of the market at a specific point in time.

Without those other two data points of 1) market level and 2) point in time (which is commonly referred to as the “effective date,” meaning the date the appraised value is effective for), any number that is thrown around as a value is essentially meaningless.

Based on this, the same exact object can have multiple values on the same day, depending on what level of the market one is evaluating. An appraised value for insurance may be significantly higher than an appraised value for planned future sale, which can be baffling and difficult to comprehend without a familiarity with the different levels of the market.

For those without dedicated appraisal training, and especially for those in the general public who may be thinking of having items appraised, these concepts are often unknown and frequently very confusing. I’ve written this basic guide as an introduction to the different levels of value so that users of appraisal services will be able to better determine what sort of appraisal reports would best suit their needs. To be clear, the levels I am describing are those typically used in the United States, where I am based, but I recognize that among our international readership there may be other levels of value specific to different countries.

All appraisal reports written in compliance with the Uniform Standards of Professional Appraisal Practice (USPAP) have to include identification of the level of the market the appraised values are set in and the effective date of the valuation. There are a number of professional organizations for appraisers, and regrettably, they don’t all use the same terminology to describe the different levels of the market. For the purposes of this guide and to improve clarity for a general audience, I have streamlined and simplified some of the names of the market, particularly for the retail market, but readers should be aware that their appraiser may use slightly different terms depending on that appraiser’s professional memberships.

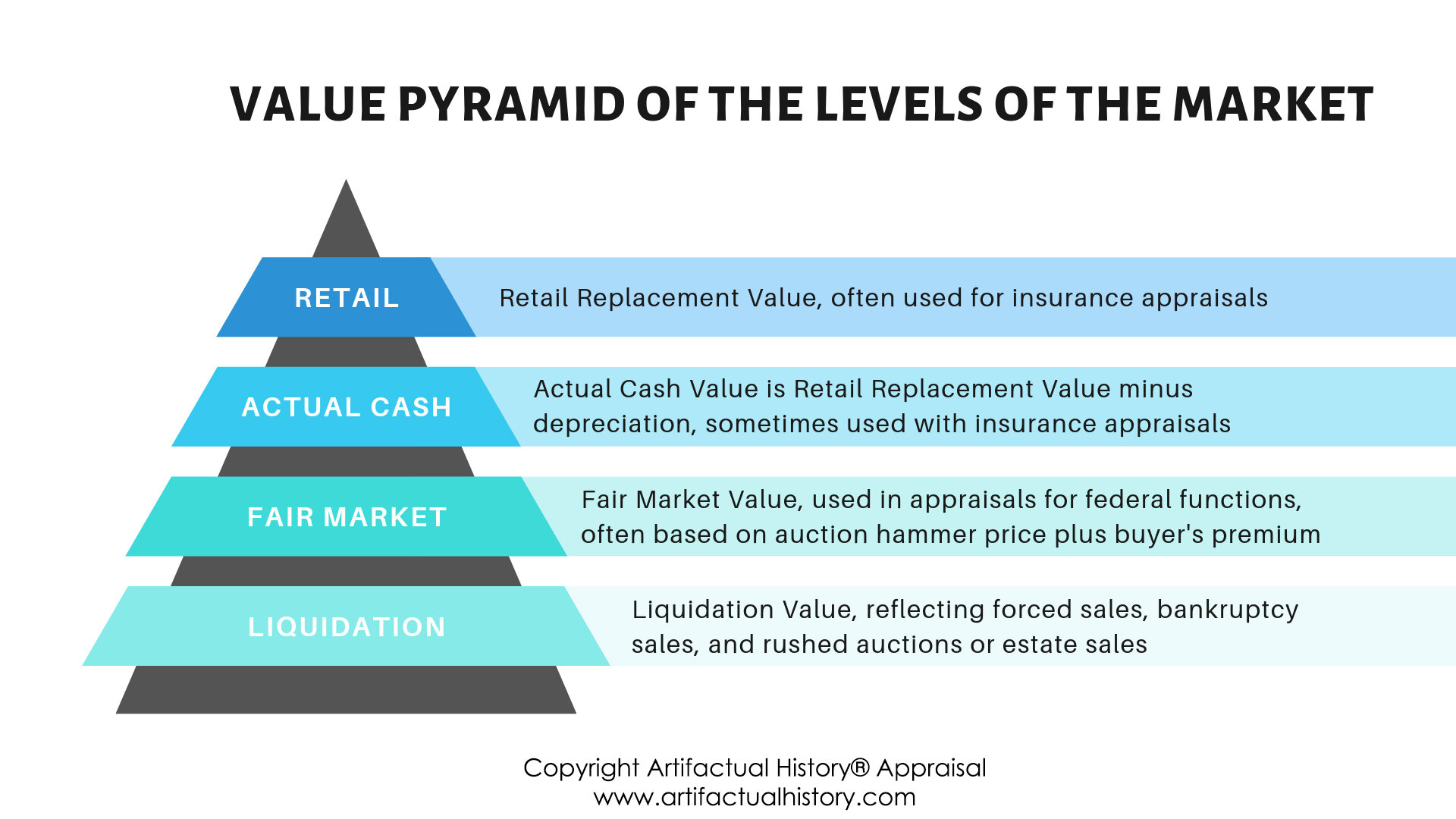

Below I will introduce the different major levels of the market working from highest to lowest, and discuss the appraisal purposes, or intended uses, that are frequently associated with certain market levels. While there are a number of other rarely used levels, in this guide I’ve focused on the main, most commonly used levels.

As defined by the Appraisers Association of America, appraised "retail replacement value" is defined as the highest amount in terms of US dollars that would be required to replace a property with another of similar age, quality, origin, appearance, provenance, and condition within a reasonable length of time in an appropriate and relevant market. When applicable, sales and/or import tax, commissions and/or premiums are included in this amount.” (Appraising Art: The Definitive Guide to Appraising the Fine and Decorative Arts, 2013, Appraisers Association of America, page 438.) You may also see this level of the market described as “replacement cost,” which is a term used by the International Society of Appraisers.

Examples of retail replacement value are the price an art gallery asks for a painting in their inventory, the asking price of a table by a furniture designer, or the manufacturer listed price of a sterling silver serving item. The key elements of the definition of retail replacement value are “the highest amount… that would be required to replace a property with another of similar [characteristics] within a reasonable length of time.” This is because retail replacement value is typically used in insurance appraisal reports, and in the event of loss, the client needs to receive a settlement from the insurance company that is sufficiently high to replace the lost items with similar replacements in a relatively short time frame. The best availability of inventory to accomplish this is within the retail market. While it might be possible to scour the auction market for years searching for an offering similar to the lost item and then obtain that item at a much lower price, this is not the function of insurance coverage. Clients pay the insurance premium precisely to preserve the option of receiving a settlement sufficient to replace items within a practical time frame sourcing from the retail level of the market.

Due to these factors, retail pricing tends to be much higher than the other levels of the market, and it can contribute to misleading expectations of the profit in a planned future sale if retail replacement values are the assumed future sale price. Most people selling items on the secondary market who aren’t professional dealers or without access to the assistance of professional dealers will find it difficult to obtain retail prices in a sale, and can more realistically expect future sale prices to be closer to the Fair Market Value and Liquidation Value levels of the market. Part of the reason retail prices are so much higher than the other levels of the market is that they reflect the overhead and carrying costs of the gallery or dealer maintaining the instant availability of the item. A gallery may have to wait years before selling a painting in its inventory, and in that intervening time the gallery would be paying rent or a mortgage for the gallery space, utilities, taxes, advertising, employee payroll, and insurance for the works in the gallery’s inventory. All of those costs are factored into retail prices and contribute to their position at the top of the levels of the market.

The next level down of value is Actual Cash Value. Actual Cash Value is Retail Replacement Value minus depreciation, which can be a deduction made for age, damage, or another factor. It can sometimes be present in insurance policies, although in my experience it is much less frequently encountered. The best way to determine what level of value you have in your own insurance policy is to pull out and read your policy documents or call up your insurance agent to confirm. In my firm’s appraisal assignments, I’ve found that Retail Replacement Value is the main level of value used in fine art and antique insurance coverage.

The next level is Fair Market Value. Fair Market Value is used in all appraisal reports for United States government federal functions such as non-cash charitable contributions for income tax deductions and estate tax. Fair Market Value is also frequently encountered in equitable distribution and family distribution appraisal reports. The formal definition for Fair Market Value is defined by the United States government as “Appraised "Fair Market Value" is the IRS definition as stated in the Treasury Regulation Sections 1.170A-1 (c) (2) is "the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts." [Source: Treasury Regulations Sections 1.170A-1 (c) (2)]. Fair Market Values are most commonly interpreted as being sourced from auction sold prices, and based on the Technical Advisory Memorandum 9235005 [May 27, 1992], fair market value should include both auction hammer price and buyer's premium.

So what does this mean in plain language if you aren’t familiar with the auction world? The following is the example I use with clients:

Imagine you are watching an auction, and the auctioneer is up at the podium holding a wooden gavel selling a particular item. The auctioneer takes bids from all the bidders interested in the item, and the numbers of the bids continue to climb until there is a single final winning bidder. The auctioneer hammers down the wooden gavel and shouts, “Sold! $400 to Bidder A.” That $400 is called the hammer price, referencing the tradition of the wooden gavel. If Bidder A wants to remove the item from the auction house, in most circumstances it is going to cost more than $400 to be able to do so. Most auction houses also charge what is called buyer’s premium, which is a surcharge on top of the hammer price paid by the winning bidder. 25% is a common buyer’s premium across the industry. In this imagined scenario, Bidder A pays $400 plus a buyer’s premium of 25% of $400, which is an extra $100. When Bidder A pays, the total hammer price plus buyer’s premium will be $400 + $100 = $500. Sales tax is not included in the calculation of fair market value, although Bidder A may have had to pay it!

If you believe you need an appraisal written at fair market value for a legal use such as equitable distribution or family distribution, I recommend confirming this with the lawyer representing you before engaging an appraiser, as well as establishing the effective date the appraiser must write the report to. The website of the Internal Revenue Service also contains a wide range of publications providing detailed guidance about their requirements for different situations.

The final level of value to be discussed is Liquidation Value. This is the lowest level of the market discussed here and represents the price realized in a forced sale within a short time that is lacking adequate advance marketing. Due to the rushed timeline and the limited buyers who would be informed of the sale at short notice, prices are very low. A critical difference between a sale at liquidation value and a sale at fair market value is that the liquidation value sale does not have a willing seller, but rather one who is forced to sell by extenuating circumstances. Liquidation Value is often used in bankruptcy contexts.

If you aren’t sure which level of value you need an appraisal report written at, I recommend discussing your needs with the appraiser you are engaging for guidance. Many of my clients reach out to me not quite sure what they need and our subsequent discussion of the appraisal scope of work clarifies what type of report will be best suited for their situation. Users of appraisal services should feel empowered to actively ask questions about how their needs can best be met.